Topic Brief: Full course at a special price of only $10.00 found here: ($39 value).

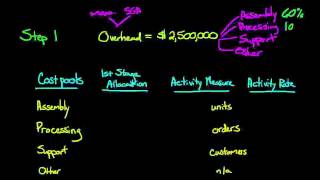

Cost Allocation Step Method -

Reflection & Clarity Considerations for this topic.

Important details found

- Full course at a special price of only $10.00 found here: ($39 value).

Why this topic is useful

A structured page helps reduce disconnected snippets by grouping the main subject with context, examples, and nearby entries.

Sponsored

Frequently Asked Questions

Is the information always complete?

Not always. Some topics may need verification from official or primary sources.

How should readers use this information?

Use it as a starting point, then open related pages for more specific details.

What should readers check next?

Readers should check related pages, official references, or updated sources when details matter.

Image References

Sponsored